Cashback Loyalty for Small Business in 2026: What's Real and What's Points in Disguise

Most 'cashback' loyalty apps for small business aren't really cashback. Here's what's real, what isn't, and what actually solves the portability problem.

Most small-business owners searching for a cashback loyalty program are looking for a way to give customers real money back on every purchase. Almost every app in the category markets itself that way. Almost none deliver it.

The most-installed Shopify loyalty apps issue points that convert into discount codes on the same store. That's not cashback. That's a discount with extra steps. A smaller wave of apps built on Shopify's 2024 Store Credit API does the accounting more honestly, but the value is still store-locked. Customers can only spend it where they earned it.

Real cashback, the kind that lets a customer withdraw earned value to their bank account or PayPal, doesn't exist in the small-business loyalty category. There's a structural reason for that, and it isn't an oversight. The business model, the regulatory regime, and the fraud surface of real cashback all work against any Shopify app that tries to deliver it. The only cashback that works the way most customers imagine it works is bank-issued: Amex Offers, Chase Offers, Capital One Offers. A small business can't deploy those.

This guide covers every option a merchant actually has in 2026, how each one really works, and what solves the portability problem cashback was supposed to solve.

What's in This Guide

- What Cashback Loyalty Actually Means in 2026: Category definitions, and where the marketing diverges from the product.

- The Points-in-Disguise Problem: Why most "cashback loyalty" isn't cashback.

- Why Real Cashback Doesn't Exist in Loyalty Apps: The business-model, regulatory, and fraud reasons.

- The 2024 Shopify Store Credit API Wave: Honest dollar math, still store-locked.

- POS Loyalty: Square, Clover, Fivestars: Same playbook in-person.

- True Cashback Platforms Don't Serve Small Business: Why Rakuten, Upside, and Ibotta aren't deployable.

- Card-Linked Offers Are Bank Products: Why Amex and Chase can, and merchants can't.

- Bitcoin Rewards: A Different Category: What actually solves the portability problem.

- Does It Actually Work?: Published research across five merchants.

- How to Choose for Your Business: Decision framework by priority.

- Frequently Asked Questions

What cashback loyalty actually means in 2026

Cashback loyalty, as most customers imagine it, means earning real money back on purchases and spending it anywhere. In small-business loyalty programs as they exist today, almost nothing works that way.

Before comparing programs, it helps to name three distinct things that marketing often uses interchangeably.

Points are conversion units. A typical Shopify program issues 5 points per $1 spent, with 100 points redeemable for $1 off a future purchase. Points expire. They're bounded by the merchant that issued them. They're structurally identical to a one-time discount, spread across visits.

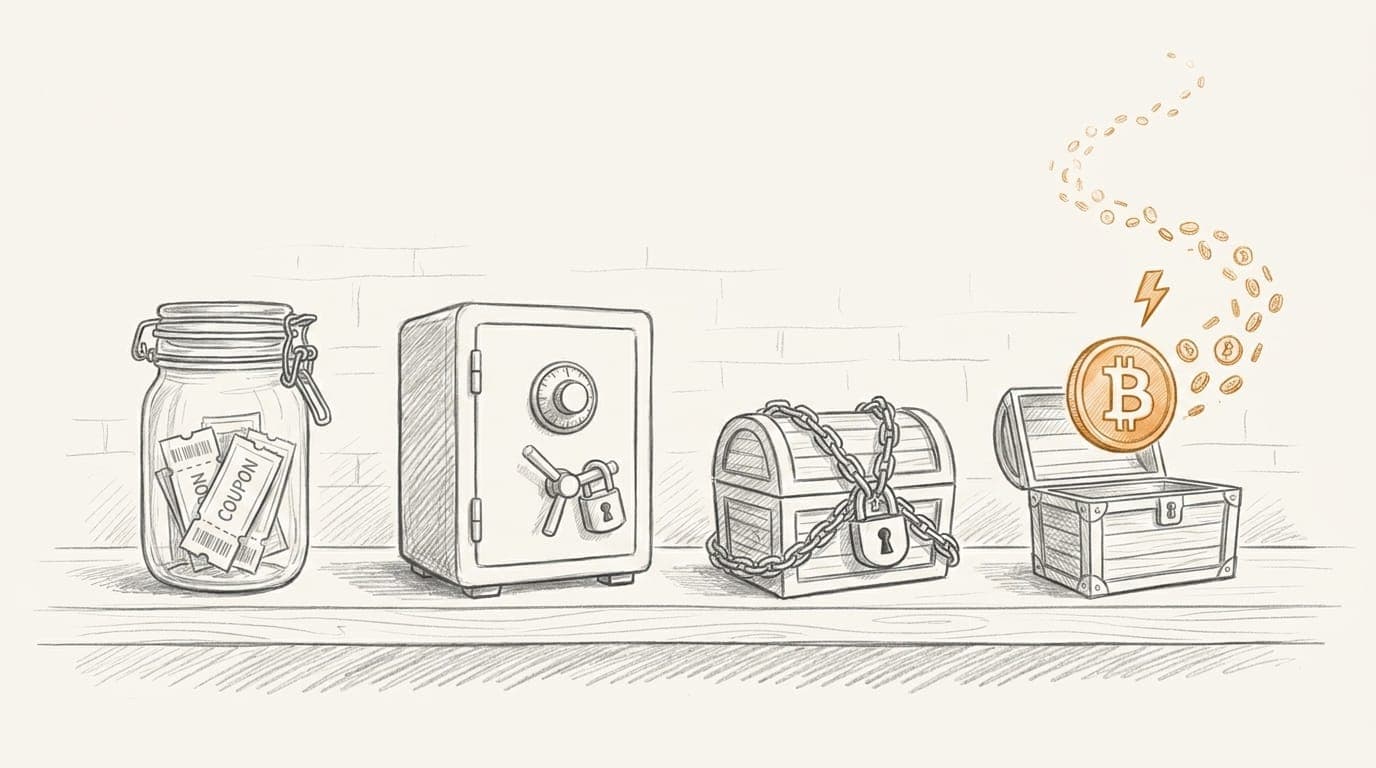

Store credit is dollar-denominated value held on the merchant's account. It passes the "real-value" test (each dollar is a dollar), but it fails portability. A customer with $40 of store credit at one shop cannot spend it at another.

Real cashback is real money, portable, and spendable anywhere. It meets all three tests: real unit of value, portable across merchants, and transferable when the customer leaves.

In small-business loyalty, real cashback is rare. When you do find it, it's almost always a bank-issued product (Amex Offers, Chase Offers) or a consumer-side ad network (Rakuten, Ibotta) that a small merchant can't deploy.

Bitcoin rewards pass all three tests in a different form. The unit isn't a dollar but a satoshi, and the customer can withdraw it off the merchant's ecosystem into their own Lightning wallet, where it holds market value that works anywhere Bitcoin works. More on this in the Bitcoin rewards section below.

The whole category at a glance:

| Type | Example | Real Value? | Portable? | Customer Can Take It? |

|---|---|---|---|---|

| Points | Smile.io, LoyaltyLion, Yotpo | No (converts to a discount code) | No | No |

| Store credit | Koin, Kash, Redeemly | Yes (dollar-denominated) | No (locked to the merchant) | No |

| Real cashback | Rakuten, Upside, Amex Offers | Yes (real money) | Yes (spendable anywhere) | Yes |

| Bitcoin rewards | Oshi | Yes (property with market value) | Yes (usable anywhere Bitcoin works) | Yes |

Bitcoin rewards share the real-cashback row on every test that matters to the customer. The only difference is the unit of value: sats instead of dollars.

The points-in-disguise problem

Most Shopify loyalty apps market themselves as cashback but issue points redeemable as discount codes. The value doesn't leave the store, and it doesn't look like the "5% cashback" on a credit card that customers assume they're getting.

The most-installed Shopify loyalty apps, with combined review counts in the tens of thousands, run variations of the same mechanic. Smile.io has over 4,000 reviews. LoyaltyLion, Yotpo, Rivo, BON, Stamped, Growave, Joy, and Gameball add thousands more. Every one of them runs points-to-discount-code redemption as the core loop. (For a traction-sorted overview, see our guide to the best Shopify loyalty apps.)

The mechanic is consistent: a customer earns points, gets an email when they're stacking up, and redeems them for a discount on a future order. The marketing calls this "rewards" or "cashback." In practice, it's a coupon with a delivery delay. Some of the larger platforms acknowledge the difference in their own educational content, drawing a line between points-based programs and real cashback, which they describe as cash or store credit rather than a redemption code.

This isn't a criticism of any one vendor. It's an honest description of what the whole category does. Shopify loyalty apps as structured today do not pay customers money. They issue points that function as merchant-controlled discounts.

The math is deliberately obscured. A program offering "5 points per $1 spent" and making "100 points worth $1 off your next order" is a 5% discount code on future purchases. The customer reads "5 points per dollar" and imagines a 5% cashback rate. The effective program is a 5% discount that materializes only when the customer returns and redeems.

For some merchants, this is fine. Discount-spread-over-time is a legitimate retention mechanic, and customers who return to collect are by definition more valuable than those who don't. The problem isn't the mechanic. It's that the mechanic is being sold under a name it doesn't deserve. (Bitcoin rewards vs traditional loyalty programs unpacks this comparison in more detail.)

If you evaluate Shopify loyalty apps assuming "I'll offer 5% cashback and customers will love it," the reality is that you'll issue a 5% discount code to customers who return and ask for it, and nothing to customers who don't.

Why real cashback doesn't exist in loyalty apps

Three structural reasons: it breaks the loyalty business model, it triggers money-transmitter regulation, and it opens a fraud surface no Shopify app is structured to absorb. Banks are the only entities positioned to offer real cashback at scale, and they do.

It breaks the business model

Loyalty programs exist to drive repeat spend. Every dollar a merchant gives away in rewards is an investment in the next purchase. Store credit preserves that dynamic: the $5 of credit a customer holds is $5 the merchant will see back on the next order. Real cash, by contrast, is $5 out of the relationship. The customer can spend it anywhere, including at a competitor. The retention math that makes loyalty worth the spend breaks when the reward is withdrawable.

It triggers money-transmitter regulation

The moment a Shopify app offers to ACH or PayPal real cash to consumers, it enters the business of moving money. In the United States, that means state-by-state Money Services Business (MSB) registration, FinCEN filings, KYC and AML compliance, and 1099 reporting above statutory thresholds. The licensing alone is a seven-figure undertaking. No loyalty app in the Shopify ecosystem is structured to absorb that cost, and none try.

This is why every app in the category, including the 2024 native Store Credit wave, delivers value in store credit rather than cash. Store credit is a promotional rebate. Cash is money transmission. The legal distance between the two is wide.

It opens a fraud surface

Withdrawable cash creates an arbitrage opportunity. Fake orders, refund-after-reward schemes, and customer-side abuse escalate quickly when earned value can be pulled off the platform. Real cashback operators absorb fraud prevention costs of 1 to 3 percent of processed volume. Loyalty apps operate on thinner margins and aren't built for that kind of exposure.

Where real cashback does work: banks

The one place in the economy where real cashback operates at scale is at the banking layer. Amex Offers, Chase Offers, Capital One Offers, and BankAmeriDeals give cardholders real dollar rebates, paid as statement credit on the card that originated the purchase. That model works because banks already carry the full fintech stack. They hold money-transmitter licenses (or are exempt under banking law), run fraud prevention at interchange scale, and have decades of regulatory infrastructure in place. A small business cannot deploy a bank-issued cashback program. It isn't a product a merchant can buy. It's a product the issuing bank offers to its own cardholders.

The 2024 Shopify Store Credit API wave

In 2024, Shopify released a native Store Credit API. A small group of apps now use it to issue dollar-denominated rewards instead of points. The math is cleaner. The value is still store-locked.

Until 2024, there was no clean way for a Shopify app to give a customer dollar-denominated credit. Every existing loyalty app built its own parallel ledger of points and handled redemption at checkout through workarounds. That's part of why points became the default.

In API version 2024-07, released in July 2024 alongside New Customer Accounts, Shopify shipped a native Store Credit primitive. A merchant or app can now issue, track, and redeem customer credit denominated directly in dollars, through the platform itself.

A small but legitimate group of apps has been built on it:

- Koin, 134 reviews, free, the only cashback-mechanic app currently in the top 20 of the Loyalty & Rewards category on the Shopify App Store.

- Kash, 113 reviews, free, with a "Built for Shopify" badge.

- Redeemly, 66 reviews, also "Built for Shopify."

- Dollarback, launched in February 2025, 22 reviews.

- Angle, an enterprise tier at $999 per month with 3 reviews but named customers including Ruffwear.

A sixth app, Rise Gift Cards & Store Credit, has been around since 2014 and holds 741 reviews. It predates the native API and proved the store-credit-over-points model long before Shopify made it easy.

What these apps get right: the dollar math is transparent. A customer earning 3% back on a $50 order receives $1.50 of credit, not 150 points that convert to $1.50 at a ratio buried in the settings. Merchants who value honesty with their customers, and customers who've been frustrated by conversion math before, can see why this is an upgrade.

What they still don't solve: portability. A customer with $40 of Koin credit at Store A cannot spend it at Store B. The credit lives inside the merchant's Shopify account. It's a walled garden with cleaner accounting.

For many merchants, that's acceptable. Store credit, by design, drives reinvestment in the store that issued it, which is exactly the retention behavior the merchant pays for. If the goal is to spread a discount across multiple future visits with honest math, native Store Credit apps deliver.

If the goal is to give customers value they can take with them, store credit is still not cashback.

POS loyalty: Square, Clover, Fivestars

Brick-and-mortar loyalty runs the same playbook. Square Loyalty, Clover Rewards, and Fivestars all issue points or store credit locked to the merchant. None let value leave the store.

The points-in-disguise pattern extends beyond Shopify into in-person point-of-sale loyalty. Square Loyalty, Clover Rewards, and Fivestars (now SumUp Reward Stamps after SumUp's 2021 acquisition) all run the same underlying mechanic. Customers earn points or punch-card credit at a specific merchant, and redemption happens at the same POS where the purchase originated. The value never leaves the store.

For Square-specific merchants looking at their options, we've covered this in more detail in our post on Square Loyalty alternatives.

For every POS category, the architecture that unlocks portability on Shopify (covered in Bitcoin rewards: a different category) works the same way in-person, because the limiting factor is the unit of value, not the channel.

True cashback platforms don't serve small business

Upside, Rakuten, Ibotta, Fetch, and similar platforms do pay real cash, but they're ad networks for major brands, not deployable loyalty tools for small businesses.

The apps that deliver real dollar cashback to consumers exist, but they're structured as ad networks rather than merchant-deployable loyalty. Upside, Rakuten, Ibotta, Fetch Rewards, Dosh (which shut down in February 2025), Drop, and Cardlytics-powered offers all share the same shape. They acquire cashback inventory from major brands at scale and deliver it to a consumer audience through their own app. The money is real and arrives via PayPal, ACH, or check, usually after a $5 to $25 minimum threshold. Customers link bank accounts or PayPal. Some require SMS verification. Ibotta requires customers to activate at least one "name-brand offer" before their first withdrawal becomes eligible.

Upside is the one partial exception on the small-business side. It onboards independent merchants, but only in specific verticals: fuel, convenience, grocery, and restaurants. An independent Shopify store selling physical goods online cannot participate.

For everyone else, the cashback inventory these networks serve is supplied by major brands, paid for by the brand's marketing budget, and delivered to the consumer with the network taking a margin. The small business is neither the buyer nor the seller. This isn't a loyalty category for independent merchants. It's an advertising category for large ones.

If you've searched "cashback rewards" and found results that look like consumer apps, this is why. They're real cashback. They're just not yours to deploy.

Card-linked offers are bank products

Card-linked offers are real cash rebates, but they're issued by banks to their own cardholders. Small merchants generally can't deploy them, and most consumers only see them if they hold the right card.

Amex Offers, Chase Offers, Capital One Offers, BankAmeriDeals, and similar card-linked offer (CLO) programs deliver real cashback to cardholders as statement credit. A cardholder activates an offer in their banking app, makes the qualifying purchase, and sees the rebate arrive on their next statement (or up to 90 days post-offer-end for Amex, up to three billing cycles for Capital One).

The offers themselves are typically bought by national brands through Cardlytics or similar ad tech, in partnership with the issuing bank. Capital One Offers explicitly excludes small-business cards from its program. Small merchants generally cannot directly buy CLO inventory, and when they can, the setup requires a relationship with Cardlytics that exceeds most independent businesses' capacity.

Two takeaways matter for this post. First, CLO cashback is real cashback, structured to work without becoming money transmission, because the bank is already licensed for it. Second, CLOs are a bank product, not a small-business loyalty primitive. Reading about them doesn't help a merchant looking to set up a rewards program on their own store.

Bitcoin rewards: a different category

Merchant-funded Bitcoin rewards sidestep the structural problems of cashback by changing the unit of value. The reward is Bitcoin (property, not currency), paid in small amounts through the Lightning Network. Customers can redeem inside the merchant for an enhanced rate, or withdraw to any Lightning wallet. It isn't cashback, and it's the only small-business loyalty primitive that delivers portable value.

So far, every category this post has covered either delivers non-portable value (points, store credit, POS stamps) or can't be deployed by an independent small business (consumer cashback apps, card-linked offers). For merchants who want to offer customers something genuinely portable, something a customer can take with them and use anywhere, one approach works: change the unit.

Merchant-funded Bitcoin rewards, like the programs deployed through the Oshi platform, issue rewards in sats (satoshis, the smallest unit of Bitcoin) instead of dollars or points. That single substitution unlocks a structurally different program. For the product-side view of how this works in practice, see our Bitcoin Back feature page.

Why changing the unit works

Property, not currency. Bitcoin is classified as property under IRS Notice 2014-21. Merchant-funded Bitcoin rewards are promotional consideration paid in property, not monetary payouts. That keeps the merchant and the platform out of money-transmitter territory that would kill any fiat-cashback Shopify app.

Small amounts, Lightning rails. Rewards are typically 1 to 5 percent of each purchase, paid in sats through the Lightning Network. Lightning delivers value instantly and at negligible cost, without bank integration, without minimum thresholds, without Plaid or ACH. The customer doesn't link a bank account. They never have to.

Dual-mode redemption. This is the feature that makes the model work for both sides of the relationship. Customers have two redemption paths:

- Redeem back on the merchant at an enhanced multiplier. Sats recycled into a store discount are worth more than they'd be worth as a withdrawal. This preserves the store-credit reinvestment dynamic merchants care about.

- Withdraw to any Lightning wallet. A customer with an earned balance can pull those sats off the platform entirely, into their own wallet. From there, the value is theirs to spend, hold, or use anywhere Bitcoin works. Many customers use widely-adopted apps like Cash App or a Bitcoin exchange account as their Lightning endpoint, where sats arrive like any other Bitcoin balance and can be held or sold for dollars. That last step isn't something the merchant or the rewards platform handles. It's something the customer does with their own wallet or exchange, the same way they would with any Bitcoin they bought themselves.

The network effect points programs can't replicate

Points and store credit are inherently single-merchant. Value earned at Store A only works at Store A. That's fine for retention, but every loyalty program exists as an island.

Bitcoin rewards change this. Because the unit of value is portable, the same reward customers earn at one merchant works the same way at every other merchant on the platform. That unlocks a marketplace effect points programs can't replicate. The Bitcoin Rewards marketplace is a directory of merchants offering Bitcoin rewards, and customers actively browse it to discover new businesses because the sats they earn at a new merchant stack with what they've already earned elsewhere. The Oshi Network side of this connects merchants to Bitcoin-focused directories, podcasts, and communities that drive traffic to merchants in the marketplace.

For a merchant, this is an acquisition channel, not just a retention mechanic. Points programs retain existing customers. Bitcoin rewards retain existing customers and expose the merchant to a community that actively seeks them out. Early merchants benefit most because the network compounds: more merchants make the marketplace more useful to customers, which brings more customers, which makes the marketplace more valuable to join.

What this looks like in practice

Merchants like Peony Lane, a Colorado high-altitude winery, and Farmer Bill's Provisions, a South Dakota brand making biltong and steak sticks from regenerative pasture-raised beef, run merchant-funded Bitcoin rewards on their stores today. Both use the dual-mode architecture. Customers earn around 1% back in sats on every order, accumulate rewards across purchases, and choose how to use them.

Positioning honestly

This isn't cashback, and we're careful not to call it that. The Oshi platform is explicitly not a bank, not a cryptocurrency exchange, not a wallet provider, and not a money transmitter. Sats are a conditional right to receive Bitcoin, not stored cash. Customers earn, claim, and either redeem or withdraw to a Lightning wallet, in that sequence of verbs.

As of 2026, Oshi is effectively alone in the category of small-business loyalty platforms that issue rewards in portable value rather than store-locked points or credit. That's the result of a narrow architectural window: the unit substitution to Bitcoin, small per-purchase amounts, Lightning rails for reward delivery, and a dual-mode redemption that preserves merchant economics.

Whether it's the right fit depends on what you're actually trying to do.

Does it actually work?

Yes, according to published research on five Oshi merchants. Enrolled customers return faster and spend more than non-enrolled customers, with effects that hold across product type and customer cohort.

Oshi's published customer-behavior research tracks enrolled-versus-non-enrolled customers across five merchants in different categories: beef jerky, supplements, liquid vitamins, skincare, and provisions.

Headline findings:

- Faster return. After enrolling, customers cut their purchase gap by three or more days. Non-enrolled customers over the same period actually slow down, widening the divergence.

- Higher spend. Enrolled customers outgrow non-enrolled comparison groups by a meaningful margin on a per-customer basis.

- Consistency. The effect holds across all five merchant types, at every enrollment timing (second visit, third, fourth, and later), and survives stress tests like removing the top 1% of outliers.

- Honest uncertainty. The research disclosure estimates 70 to 75 percent confidence in the causal interpretation, acknowledging that self-selection (more-loyal customers may be more likely to enroll) accounts for some of the gap.

For merchants evaluating any loyalty mechanic, this is the kind of evidence to look for before committing budget. For more on how to measure loyalty program impact, see our loyalty program effectiveness research.

How to choose for your business

The right program depends on whether you prioritize simplicity, honest accounting, or portable value. Here's a decision framework.

| If you want customers to receive... | Best fit | Examples |

|---|---|---|

| Points redeemable for a discount code on your store | Points loyalty apps | Smile.io, BON Loyalty, LoyaltyLion |

| Dollar-denominated store credit, no conversion math | Native Store Credit apps | Koin, Kash, Redeemly, Rise Gift Cards |

| Real cash to customer bank accounts | Not available as a small-business product | Bank-issued cards (Amex, Chase) or consumer cashback networks (not merchant-deployable) |

| Portable, non-store-locked value customers can take with them | Bitcoin rewards | Oshi on Shopify |

| Both store reinvestment and a portable option | Bitcoin rewards with dual-redemption | Oshi |

All of these options install through the Shopify App Store with comparable setup flows. The honest decision axis isn't implementation complexity, it's what customers actually receive.

A few guidance notes beyond the table.

If your customers are already crypto-literate (Bitcoin-focused brands, tech-audience products, Bitcoiner-owned businesses), Bitcoin rewards with dual-mode redemption is often the strongest fit. The portability becomes a feature customers actively want.

If your customers are mainstream and you haven't thought about Bitcoin for your business before, the decision comes down to whether you want to be among the first merchants in your category to offer portable rewards. Being first is a differentiator, and it also buys you the longest runway on the Bitcoin Rewards marketplace, where Bitcoin-focused shoppers actively seek out merchants like you.

If you run a points program already, notice how your customers talk about it, or whether they do at all. In practice, points programs tend to be invisible to customers. They've come to expect discounts in another flavor, and most don't engage with the mechanic beyond occasionally checking a balance. Many merchants who quietly switch off a points program find that customers don't say a word. That silence is the real signal. If the program isn't generating customer attention, it probably isn't creating meaningful differentiation either. Points can still function as a retention backstop, but they rarely function as something customers actively care about. Bitcoin rewards tend to go the other way, because the reward itself is novel enough to get noticed.

If you've been frustrated by points conversion math or your customers have asked for something more transparent, the native Store Credit apps are a clean upgrade from points with the same category economics.